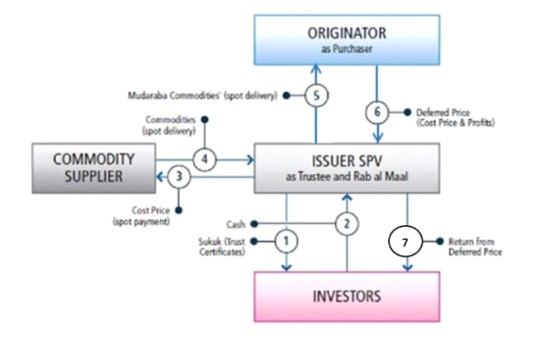

They are issued on the basis of a Murabaha contract, and the proceeds of their issuance are used by the Sovereign Taskeek Company to finance the purchase of the usufruct rights to the Murabaha assets, from a supplier or owner, for the purpose of the Sovereign Taskeek Company selling this right to the issuing party. The Suk represents a common share in the ownership of the usufruct rights to the Murabaha assets after purchasing it from the supplier or owner, then in its price that must be paid by the issuing entity to the sovereign Taskeek company, and the return of these sukuk is the difference amount between the purchase price of the usufruct right paid by the sovereign Taskeek company to the supplier or owner, and the price of its sale, which the issuing entity is obligated to pay to the sovereign Taskeek company, and the issuing party may sell the purchased usufruct to others.

Ijarah Sukuk

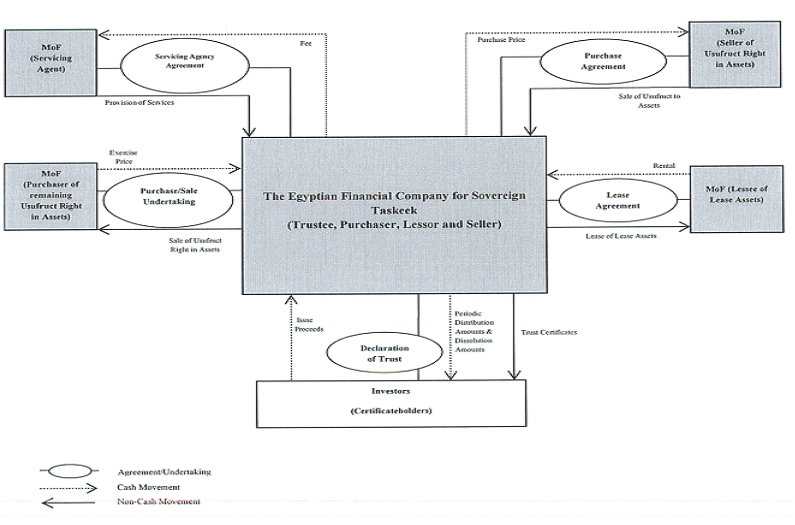

They are issued on the basis of a contract that includes the transfer of the assets usufruct right, concluded between the issuing entity and the sovereign Taskeek company, with the intention of leasing them to the issuing entity under a leasing contract. The suk represents a common share in the usufruct right, and the return on these Sukuk is due from the lease value paid from The issuing entity under the lease contract.

Istisna’ Sukuk

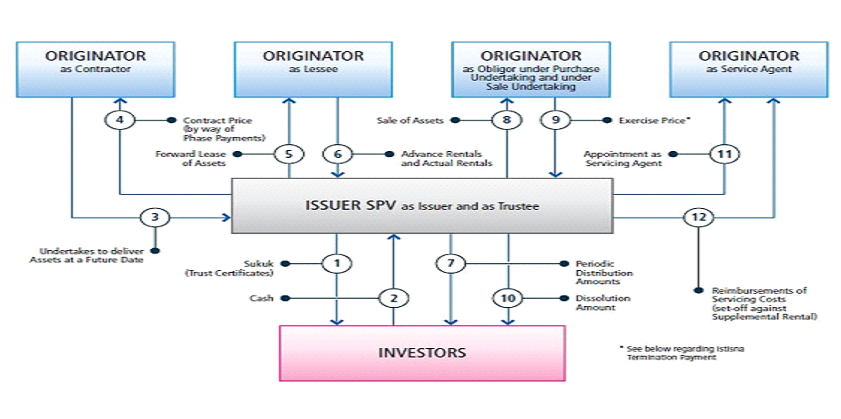

They are issued on the base of manufacturing assets for the purpose of selling or leasing the usufruct rights of these assets. The suk represents a common share in the ownership of the usufruct rights of the manufactured assets, the return from these sukuk is from the net lease value or the selling price of the usufruct rights or the amount refunded from the istisna’ payments when the purchase underwriting is implemented, taking into consideration the following:

1- The istisna’ price must be known at the time of contracting, and it may be in cash, in kind, or usufruct for specified period, whether the usufruct is from the istisna asset itself or another usufruct offered by the manufacturer.

2- Istisna’ suk shall not be traded after transferring a benefit of assets to the issuing party except at nominal value and at a present value.

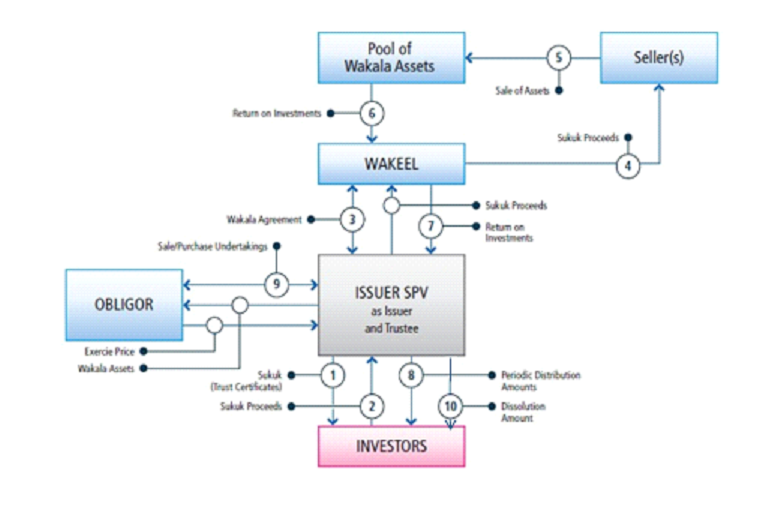

Wakkala Sukuk:

They are issued on the basis of an agency contract in investing the usufruct rights of the assets, the sovereign Taskeek company is an agent for the investment, and the owners of the sukuk are the principals, the proceeds of the sukuk are the invested amount by the agent, and the sukuk represents a common share in the usufruct rights of the assets, the sovereign Taskeek company invests the assets by leasing it, the return on suk is the differences in value between the lease amount and the suk issuance price.