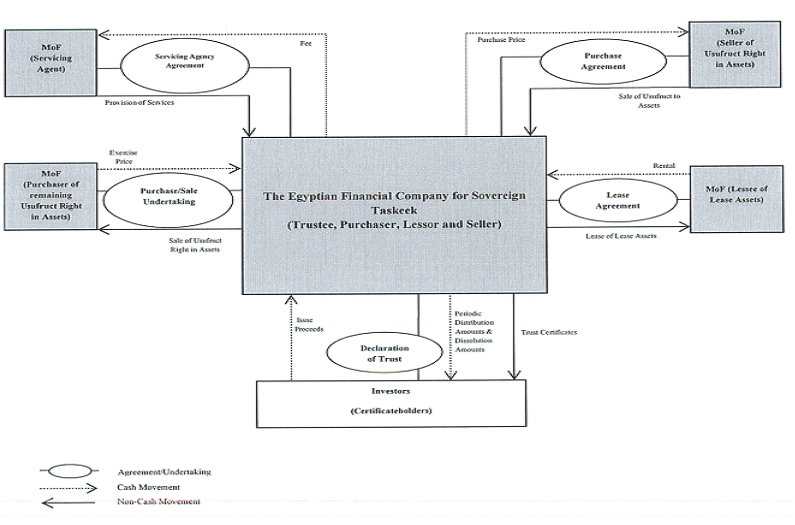

A sukuk issuing entity that owns the assets, benefits, or projects subject to financing on behalf of the sukuk holders, transfers the proceeds of the funds to the beneficiary, acts as an agent for the sukuk holders, ensures the periodic payment of returns and the payment of the redemption value when the sukuk matures.

The legal entity benefiting from the financing resulting from the taskeek process with the proceeds of the sukuk subscription and owning the assets, benefits, properties, project, and other rights. The Egyptian Capital Market Law has allowed certain entities, companies, bodies, and international or regional organizations to benefit from the financing by issuing sukuk themselves.

A bank, a licensed securities company, or any other financial institution licensed by the Financial Regulatory Authority to manage, organize, and promote the issuance on behalf of the beneficiary and the issuing party.

A bank licensed by the Central Bank of Egypt that acts as an agent for the issuing entity to coordinate the payment of the sukuk and pay their value at the end of the term to their owners or one of the companies licensed to practice the activity of depository and central registration.

A company licensed by the Financial Regulatory Authority to study the creditworthiness of the issuer of the Sukuk for the purpose of issuing a judgment indicating the extent of its ability to fulfill its obligations towards the sukuk holders. (This is with regard to corporate sukuk issuances).

While in the case of international sovereign sukuk, the sukuk is classified by international credit rating agencies.

A company or bank licensed by the Financial Regulatory Authority to provide the service of managing the sukuk records from a financial and legal perspective, and undertakes the clearing and settlement of financial positions arising from the Sukuk trading operations and the registration of mortgage rights on it. The custodian also follows up on the dues of returns for the benefit of the Sukuk holders and submits periodic reports to both the sukuk issuing company or the beneficiary party, accordingly.

He is responsible for preparing contract and agreement models and determining the legal position of each step during the issuance period.

- Sharia Supervisory Committee:

It studies and approves the various aspects of the issuance from a sharia perspective, including approving the assets subject to taskeek and approving the issuance contracts, as well as verifying the continuity of dealing in the sukuk from the time of their issuance until their value is recovered in accordance with the principles of Islamic Sharia.

- The Supreme Evaluation Committee: “In case of issuing sovereign sukuk”

It is a committee of relevant experts that specializes in evaluating the usufruct or estimating the lease value of the assets on which sovereign sukuk are issued upon. The committee is formed based on the Prime Minister`s decision.